Using Company Voluntary Arrangements to Restructure Insolvent AIM Listed Companies

In 2000, Antony Batty, one of the Licensed Insolvency Practitioners at Antony Batty and Company, pioneered the use of Company Voluntary Arrangements to reorganise and restructure AIM listed companies that had entered insolvency, enabling them to relist. This provided value for creditors and shareholders. Prior to this, the most likely outcome would have been liquidation.

This article looks in more detail at the use of Company Voluntary Arrangements in the arena of insolvent AIM listed companies, a specialism of Antony Batty and Company – click here for a recent testimonial from CogenPower PLC.

Insolvent Listed Companies Still Have Some Value

With insolvent listed companies, the very fact that they are listed means that they still have some value because of the considerable costs that are associated with gaining a new listing on the London Stock Exchange, The Alternative Investment Market or Ofex. Professional fees can run into hundreds of thousands for preparing a listing. For that reason, dormant listed companies – usually referred to as shell companies – are attractive to other companies wishing to list if they can be reversed into the shell, thus avoiding the cost of listing.

The Key is to Restore Solvency by Using Company Voluntary Arrangements

In order to realise the value of this potential asset, the shell company needs to be restored to solvency by restructuring its balance sheet. This is done through the use of company voluntary arrangements. Here, the creditors of the insolvent listed company exchange their debt for shares in the new company, under the terms of the CVA. The acquirer may also pay monies into the CVA for distribution to the creditors in addition to their receipt of shares.

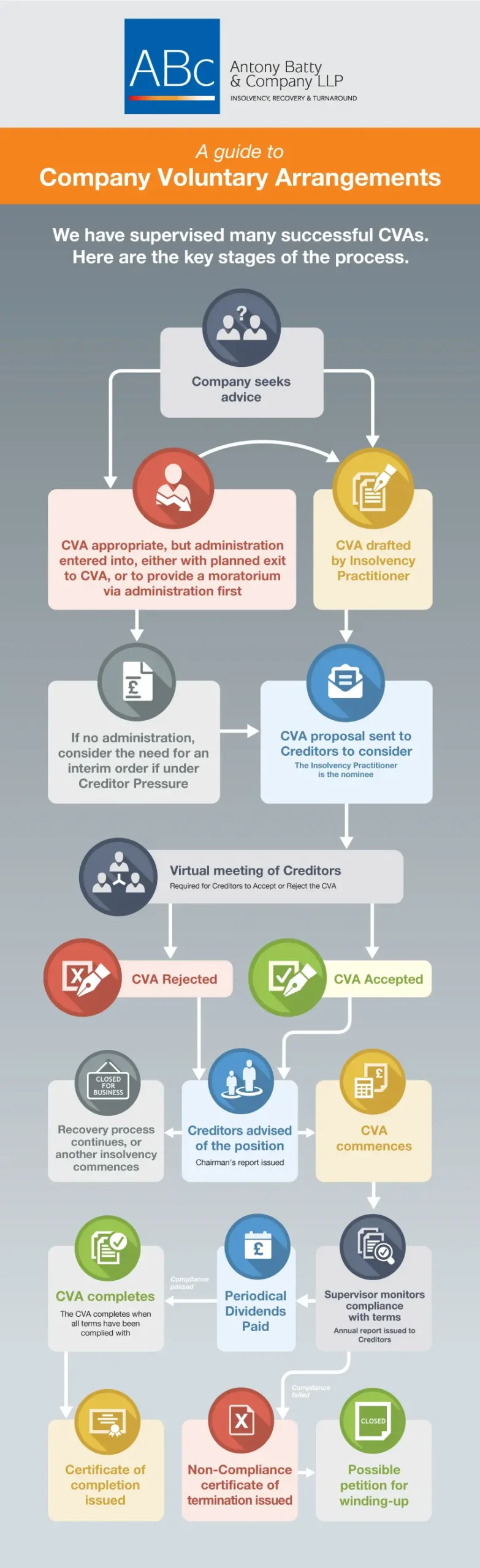

Click here for our CVA flowchart which summarises the process.

{kind=link}

How are Likely Candidates Identified?

The 3 main determinants to identify likely candidates are:

- The candidate must have a recently suspended listing

- It is likely that the candidate will be dormant, where the subsidiaries of a holding company are all insolvent, for example, and of no value. Alternatively, a PLC, which is in receivership, where all the assets have realised and the receivers have completed the administration.

- The shareholders must be willing to work with the Insolvency Practitioner who is supervising the CVA.

What Determines the Likelihood of Success? Specialist Knowledge is Required

Even if the above conditions are met, success is only likely if there is commercial interest in the restructured company as a shell. The main concern of the insolvency practitioner is always to restructure the company, using the CVA, to return it to solvency. However, in these situations further specialist knowledge is required:

- to arrange for the shares to be re-listed

- to place any new shares, and

- to look for potential acquisitions to reverse into the shell

This means the insolvency practitioner must work closely with the company’s brokers and other professional advisors.

What are the Requirements for a Successful Re-listing?

For the shell company to be re-listed:

- The Stock Market will require it to be solvent, meaning the CVA must be completed successfully

- The company must have sufficient working capital for at least 12 months

- It must have a broker, a market maker and, in the case of an AIM listed company, a nominated advisor.

- The market will also scrutinise the quality and capability of the board of directors

- Investors will need to be found to invest in the company in order to provide the necessary working capital

This is Where Company Voluntary Arrangements Come in

In the absence of any cash injection into the insolvent PLC or AIM listed company, a CVA is used to restore solvency in the company. CVAs allow creditors to waive their debt or exchange it for shares on the basis that the re-listed company can be easily sold. It is for this reason that CVAs involving debt for equity swaps offer creditors some degree of recovery. If the company was liquidated instead, no funds would be available to the creditors.

Contact us for More Details on the use of Company Voluntary Arrangements in Insolvent Listed Companies

[cta-cva]

AIM listed company insolvencies and the use of Company Voluntary Arrangements require the insolvency practitioner to have specialist expertise. Antony Batty & Company has that specialist expertise, and has assisted more than 20 AIM listed companies restructure and re-list successfully.

Contact Antony Batty or call us on 0208 088 0633 for more details on this specialist area of insolvency. The initial discussion is FREE. With offices in Central London, Essex and Salisbury, we have good coverage of the country.